Breaking down your Auto Insurance Coverage

Auto liability insurance is a legal requirement in most states, but many car owners don’t fully understand what their policy covers. Essentially, it’s insurance that pays for damages or injuries you might cause to others while driving. It can help protect you from potentially ruinous legal and financial consequences in the event of an accident. But what exactly does it cover? And what are the limits of liability insurance? In this blog post, we’ll take a deep dive into the specifics of auto liability insurance, so you can make informed choices about your coverage.

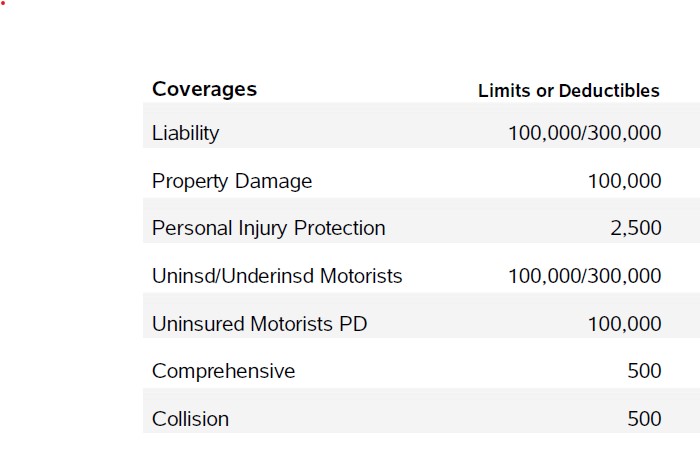

When you receive an insurance quote, you will receive all of the following information.

What is Auto Liability Insurance?

Auto liability insurance is a type of car insurance policy that covers you in the event of an accident that is your fault. If you cause an accident and someone is injured or their property is damaged, your liability insurance will pay for their damages up to your policy limits.

Liability insurance is divided into two types where most states require a minimum amount of each type of coverage.

- Bodily Injury Liability (BIL), typically called Liability : BIL covers costs associated with injuries or death

- Property Damage Liability (PDL): while PDL covers damages to someone else’s property, such as their car or home.

How Does Liability Insurance Protect You?

Auto liability insurance can protect you from potentially ruinous financial consequences in the event of an accident. If you cause an accident and someone is injured or their property is damaged, your liability insurance will pay for their damages up to your policy limits.

If you don’t have liability insurance and you’re at fault in an accident, you could be sued for damages and forced to pay out of pocket. This could lead to financial ruin, especially if the damages are substantial.

What is Personal Injury Protection (PIP)?

Personal Injury Protection (PIP) is a type of insurance that provides coverage for medical expenses, lost wages, and other expenses related to injuries sustained in a car accident, regardless of who is at fault for the accident.

In some states, PIP coverage is mandatory, while in others, it is optional. The extent of coverage and the specific benefits provided can vary depending on the insurance policy and the laws of the state in which the policy is issued.

PIP typically covers:

- Medical expenses: This includes costs for medical treatment, hospitalization, surgery, rehabilitation, and other necessary medical services related to injuries sustained in a car accident.

- Lost wages: PIP may reimburse policyholders for a portion of the income lost due to being unable to work because of injuries sustained in a car accident.

- Funeral expenses: In the unfortunate event of a fatal accident, PIP may cover funeral and burial expenses.

- Essential services: Some PIP policies may cover expenses for necessary services, such as childcare or household chores, that the injured person is unable to perform due to their injuries.

PIP is often referred to as “no-fault” coverage because it provides benefits regardless of who is responsible for the accident. This means that even if you caused the accident, you can still make a claim under your own PIP coverage for your injuries and related expenses. However, the specifics of PIP coverage can vary significantly depending on the state in which you reside and the terms of your insurance policy.

What are the Limits of Liability Insurance?

Auto liability insurance policies have limits, which represent the maximum amount the insurance company will pay for damages or injuries you cause in an accident.

Limits are typically expressed as three numbers, such as 25/50/25.

- The first number (25) represents the maximum amount the insurance company will pay for bodily injury per person

- The second number (50) represents the maximum amount the insurance company will pay for bodily injury per accident

- The third number (25) represents the maximum amount the insurance company will pay for property damage per accident.

It’s important to choose liability insurance limits that are appropriate for your financial situation and risk tolerance.

What Does Liability Insurance Not Cover?

Auto liability insurance does not cover damages to your own vehicle or injuries to yourself or your passengers in the event of an accident.

For these types of losses, you’ll need additional coverage, such as collision or comprehensive insurance.

Liability insurance also does not cover intentional acts or criminal behavior, such as driving under the influence of drugs or alcohol. If you engage in these types of behaviors, your liability insurance will likely be void, and you could be held personally responsible for any damages or injuries.

How Much Liability Insurance Should You Have?

The amount of liability insurance you should have depends on your personal situation.

State minimums may be enough for some drivers, but if you have significant assets or a high net worth, you may want to consider purchasing additional liability insurance to protect your assets in the event of a lawsuit.

The state minimums are:

MD: 30/60/15

VA: 30/60/20

DC: 25/50/10

You may also want to consider an umbrella policy, which provides additional liability protection over and above your auto liability insurance limits.

Auto liability insurance is a crucial form of protection for car owners, but it’s important to understand what your policy covers and what it doesn’t. By understanding the basics of liability insurance, you can make informed decisions about the amount of coverage you need to protect yourself and your assets.

Remember, the cost of not having enough liability insurance can be devastating in the event of an accident. So, take the time to review your policy and ensure that you have the appropriate amount of coverage to meet your needs.

Reach out to Gordon Insurance to review your existing policy or talk about a new policy.