Navigating auto insurance options can be confusing. One term you might encounter is “CSL insurance,” also known as “combined single limit” or “500/500.” But what exactly does CSL insurance mean, and how does it differ from other coverage options? This comprehensive guide will break down everything you need to know about CSL coverage, empowering you to make informed decisions for your auto insurance needs.

What is CSL Insurance?

CSL (Combined Single Limit) insurance is a type of auto insurance coverage that combines your bodily injury liability coverage into a single limit. This limit applies to both the total amount your insurance company will pay per accident for all injuries sustained by others involved (including passengers), and the maximum payout per person.

For example, if you have a CSL policy with a limit of $500,000, this means your insurance company will pay a maximum of $500,000 for all bodily injuries arising from a single accident, regardless of how many people are injured. The coverage can also be further divided, such as $250,000 per person and $500,000 per accident.

Key Features of CSL Insurance

- Single Limit: CSL coverage simplifies things by offering one limit for both total bodily injury payout per accident and per person injured.

- Flexibility: CSL policies come in various coverage limits, allowing you to choose the level of protection that aligns with your budget and risk tolerance.

- Cost-Effectiveness: CSL coverage can sometimes be more affordable than split limit policies, especially for low coverage limits.

CSL Insurance vs. Split Limit Coverage

While CSL offers a straightforward approach, it’s important to understand how it compares to split limit coverage, the more traditional option. Split limit policies provide separate limits for bodily injury liability coverage:

- Per-Person Limit: This limit applies to the maximum payout your insurance company will provide for injuries sustained by a single person in an accident.

- Per Accident Limit: This limit represents the total amount your insurance company will pay for all bodily injuries arising from a single accident, regardless of how many people are involved.

For instance, a split limit policy might offer $250,000 per person and $500,000 per accident. This means your insurance company would pay a maximum of $250,000 for each injured person, up to a total of $500,000 for all injuries in a single accident.

Table 1: CSL vs. Split Limit Coverage

Feature | CSL Coverage | Split Limit Coverage |

Bodily Injury Liability Coverage | Single Limit for Total & Per Person | Separate Limits for Per Person & Per Accident |

Flexibility | Limited Coverage Options | Wider Range of Coverage Options |

Cost | Potentially More Affordable (for low limits) | Varies Depending on Chosen Limits |

When is CSL Insurance a Good Choice?

CSL insurance might be a suitable option for you in the following scenarios:

- Limited Budget: If you’re on a tight budget and prioritize affordability, CSL can offer lower premiums compared to split limits with similar overall coverage.

- Low-Risk Driver: If you have a clean driving record and consider yourself a low-risk driver, the likelihood of causing an accident with multiple severely injured people is relatively low.

- Minimal Assets: For individuals with minimal assets, a CSL policy with a lower limit might be sufficient to protect them from financial repercussions in case of an accident.

Important Considerations Before Choosing CSL Insurance

While CSL offers benefits, it’s crucial to weigh the potential drawbacks before making a decision:

- Limited Coverage in Serious Accidents: If you cause a severe accident with multiple people sustaining serious injuries, the CSL limit might not be enough to cover all medical expenses. This could leave you personally liable for any remaining costs.

- Lack of Flexibility: CSL policies typically offer fewer coverage options compared to split limits. You might not be able to customize the per-person and per-accident limits to your specific needs.

- State Requirements: Some states have minimum requirements for bodily injury liability coverage, and these might not always align with CSL limits. Ensure your chosen CSL policy meets your state’s requirements Should you consider increasing your liability limits?

Choosing the Right Coverage

Selecting the right auto insurance coverage, particularly regarding bodily injury liability, depends on your individual circumstances and risk tolerance. Here are some factors to consider:

- Driving Habits: If you frequently drive in high-traffic areas or have a history of accidents, opting for higher coverage limits might be prudent.

- State Minimums: Each state mandates minimum liability coverage limits. Ensure your chosen policy meets or exceeds these requirements. You can find your state’s minimums on the website of your state’s Department of Motor Vehicles (DMV).

- Assets: Individuals with significant assets (e.g., house, savings) are more vulnerable to lawsuits in case of an accident exceeding their insurance coverage. Higher limits can provide greater protection for your assets.

CSL vs. Split Limits: A Deeper Look

Let’s delve deeper into the advantages and disadvantages of CSL and split limit coverage to aid your decision-making:

Advantages of CSL Insurance:

- Simplicity: CSL offers a single limit, eliminating confusion about separate per-person and per-accident limits.

- Potentially Lower Cost: For low coverage limits, CSL can be more affordable than split limits.

Disadvantages of CSL Insurance:

- Limited Coverage in Major Accidents: The single limit might be insufficient to cover all medical expenses if you cause a severe accident with multiple injuries.

- Less Flexibility: CSL options often have fewer coverage limit variations compared to split limits.

Advantages of Split Limit Coverage:

- Customization: Split limits allow you to tailor coverage to your needs. You can choose higher per-person limits to protect against severe injuries and a lower per-accident limit to manage costs.

- Potentially More Affordable for High Coverage: For high coverage needs, split limits can sometimes be more cost-effective than CSL, as you can adjust the per-accident limit without necessarily raising the per-person limit as much.

Disadvantages of Split Limit Coverage:

- Complexity: Understanding separate per-person and per-accident limits can be slightly more complex.

- Potential for Insufficient Coverage: If you underestimate the per-accident costs, the split limits might not provide adequate protection.

Additional Considerations

- Medical Costs: Medical expenses can be substantial, especially for serious injuries. Consider the rising cost of healthcare when choosing coverage limits.

- Umbrella Insurance: An umbrella policy provides additional liability coverage beyond the limits of your auto insurance policy. It can be a valuable safeguard for individuals with significant assets.

CSL insurance offers a simplified approach with potentially lower costs for low coverage needs. However, split limits provide more flexibility and might be more suitable for high coverage requirements or those seeking customization.

Carefully evaluate your driving habits, state minimums, assets, and risk tolerance before making a decision. Consulting with a licensed insurance agent can be beneficial to determine the most appropriate coverage options for your specific situation.

Understanding Your Limits: Beyond CSL and Split Coverage

While CSL and split limits are the most common options for bodily injury liability coverage, it’s important to understand the different components that make up these limits:

- Bodily Injury Per Person (BI Per Person): This represents the maximum amount your insurance company will pay for injuries sustained by a single person in an accident, regardless of the number of people involved.

- Bodily Injury Per Accident (BI Per Accident): This represents the total amount your insurance company will pay for all bodily injuries arising from a single accident, regardless of how many people are injured.

Understanding these components is crucial for making informed choices, especially when considering higher coverage limits.

- Higher BI Per Person: This is beneficial if you’re concerned about the potential for severe injuries in an accident. For instance, if you cause an accident where one person sustains life-altering injuries, a higher BI per person limit can help ensure their medical expenses are covered.

- Higher BI Per Accident: This is advisable if you frequently drive in high-risk situations or are concerned about the possibility of multiple injuries in an accident. A higher BI per accident limit can provide more comprehensive coverage in such scenarios.

Beyond CSL and Split Limits: Additional Coverage Options

While CSL and split limits are widely used, some insurance companies might offer additional coverage options for bodily injury liability:

- Combined Single Limit with Split Per Person: This combines a single limit for the total bodily injury payout per accident with separate limits for bodily injury per person.

- Excess/Umbrella Coverage: An umbrella policy acts as an additional layer of protection that kicks in after your auto insurance policy reaches its limits. It can provide significant financial protection in case of a major accident with substantial liability costs.

Remember: Regardless of the type of bodily injury coverage you choose, it’s vital to ensure your limits are adequate for your needs. Consulting with a licensed insurance agent can be highly beneficial. They can assess your risk factors, state requirements, and budget to recommend the most suitable coverage options for your specific situation.

Taking Control of Your Coverage

Understanding CSL insurance, split limits, and their components empowers you to make informed decisions about your auto insurance policy. By carefully considering your driving habits, risk tolerance, and state minimums, you can choose the coverage that best protects you financially in the event of an accident.

Don’t hesitate to consult us at Gordon Insurance LLC. We’re here to help you navigate your auto insurance options and ensure you have the peace of mind that comes with proper coverage.

Statistics and Infographics to Consider

While we’ve explored the different coverage options, statistics can provide valuable insights to help you visualize the potential risks and benefits. Here’s an infographic outlining key statistics on bodily injury claims in the United States:

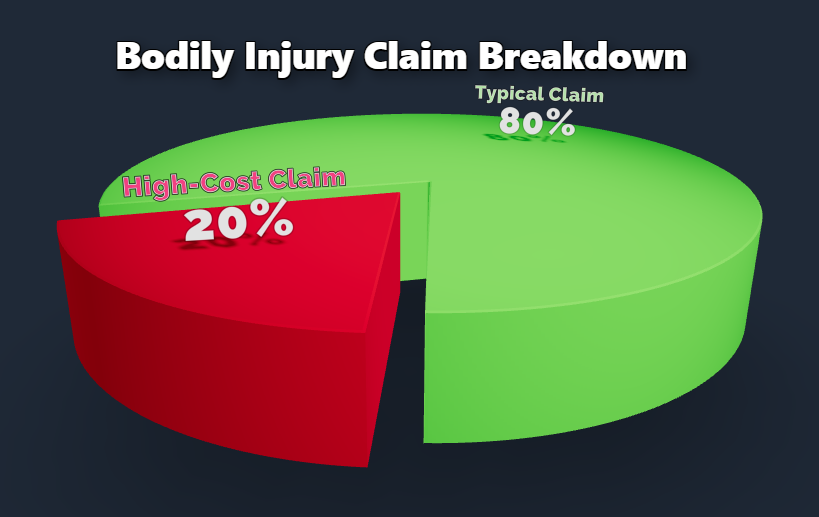

- Average Cost of Bodily Injury Claim: $51,000 (Source: Insurance Information Institute)

- Percentage of Claims Exceeding $100,000: 20% (Source: National Association of Independent Insurers)

- Impact of Multiple Injuries: Accidents with multiple injuries can significantly increase claim costs.

Considering these statistics can help you determine the appropriate coverage level for your needs. For instance, if you’re concerned about the potential for high medical expenses, opting for higher bodily injury limits might be prudent.

Additional Resources

Throughout this guide, we’ve mentioned some resources to further your understanding of auto insurance:

- Your State’s Department of Motor Vehicles (DMV) Website: This website provides information on your state’s minimum liability coverage requirements.

- Insurance Information Institute (III): The III is a non-profit dedicated to consumer education on insurance issues. Their website offers valuable resources on auto insurance coverage. Link to Insurance Information Institute website.

- National Association of Independent Insurers (NAII): The NAII is a trade association representing independent insurance agents. Their website can be a helpful resource for finding a qualified insurance agent in your area. Link to National Association of Independent Insurers website.

Remember, Gordon Insurance LLC is here to help! Our team of experienced agents is committed to providing you with personalized guidance and ensuring you have the right auto insurance coverage for your peace of mind. Contact us today for a free quote!

By combining the information presented here with additional research and consultations with a qualified insurance professional, you can make informed decisions about your auto insurance coverage and safeguard yourself financially in case of an accident.

FAQ

CSL insurance can sometimes be cheaper, especially for low coverage limits. However, the cost can vary depending on your chosen limits and insurance company.

It depends on your risk tolerance and potential exposure. If you’re a low-risk driver and have minimal assets, a CSL policy with a sufficient limit might be adequate. However, for high-risk drivers or those concerned about substantial medical costs, split limits with higher coverage might be more appropriate.

Yes, you can typically change your coverage options during your policy renewal period. Contact your insurance agent to discuss your options and any potential cost adjustments.

You cannot legally operate a vehicle with liability coverage below your state’s minimums. In such cases, you’ll need to increase your CSL limit or explore split limits to meet the required coverage levels.

An umbrella policy can provide additional protection regardless of your bodily injury coverage type (CSL or split limits). It can be a valuable safeguard, especially for individuals with significant assets or a high-risk profile.